Who applies off-payroll working rules and how to apply them is changing. To support you with legislation changes, HMRC offer businesses help to stay compliant. Their policy paper is available here: HMRC IR35 Support We've also made a video detailing the IR35 changes. Watch the video on our YouTube channel. Off-payroll working rules Off-payroll working rules changed on 6 April 2021. The legislation HMRC made available is accessible from the HMRC website. Read Off-payroll working for clients. Workers providing services via their own PSC to a client who is: | In the public sector, or a medium or large-sized private sector company | The client decides the worker's employment status and gives the reasons for their decision. The worker can dispute the determination if they disagree with it. | | A small company in the private sector | The worker's PSC will continue to be responsible for the workers employment status. To qualify as a small organisation: A small company (subject to the Companies Act 2006) must meet two of the following criteria: - Fewer than 50 employees

- Annual turnover of less than £10.2m

- Total balance sheet assets of less than £5.1m

| Read more about the off-payroll working rules for clients. The client will assess the worker as a ‘deemed employee’ for a particular engagement. Add the worker to the payroll of the ‘Fee-payer’. The Fee-payer is the party who pays the workers PSC. It's often the client but could also be another party, such as an agency if the client doesn’t pay the workers PSC. Information about the responsibilities of the fee-payer is on the HMRC website. You can read Deemed employer responsibilities under off-payroll working rules. ▼Paying a worker under off-payroll working rules 1. Create a new deemed worker  CAUTION: If you have an existing worker who becomes a deemed worker, you must end their employment. Using the usual leaver process. Read the article Dealing with leavers . Set them up as a Deemed worker using the process below. CAUTION: If you have an existing worker who becomes a deemed worker, you must end their employment. Using the usual leaver process. Read the article Dealing with leavers . Set them up as a Deemed worker using the process below.

If off-payroll working rules apply to a worker, you must create a new employee record for them:  TIP: If you're creating a new employee record, their start date is the date they became a deemed employee. TIP: If you're creating a new employee record, their start date is the date they became a deemed employee.

- From the Employees tab, select Create Employee.

- Enter their personal details as normal.

- In the Employment Details section, enter the usual employee details. Select the Deemed Employee checkbox.

- In the Previous Tax Details section, select the Starting Basis drop-down. Select Employee Declaration: P46 - Select category below.

- Select the Circumstances category as required. Usually this is category C.

- Save your changes.

TIP: The category you select decides the worker's tax code. 2. Process your pay run You process Deemed workers in a regular pay run with the following differences: -

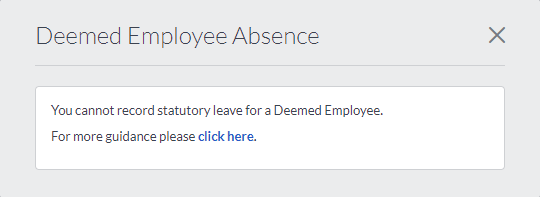

Deemed workers don't receive statutory payments. If you try to record absences for a deemed worker, you get the following message:

Exclude Deemed workers from the following deductions: - Student loan

- Automatically enrolled pension contributions

3. Submit your FPS The FPS notifies HMRC of any employee with a status of deemed. ▼What if my worker disagrees with their determination? The worker’s client decides the worker’s employment status, and if the off-payroll working rules apply. The client must then tell the worker and the fee-payer their determination and the reasons for it. If the worker or the fee-payer disagrees with the status, they can challenge it. They’ll need to write to the client to give the reasons why. Include details of: Keep copies of any records about disagreements. The client will then have 45 days from the date of receiving the disagreement to respond. During that time, pay the worker in line with the original determination. If the client doesn't change the worker's status, the client will have to tell the worker. If the client changes the worker's status, the client will have to tell the worker and the fee-payer. ▼Changing an employee's status from deemed to permanent If you have a deemed employee who has become a permanent worker: TIP: Their start date is the date they became a permanent employee. - Make the deemed employee a leaver. Set the finish date to the day before they become a permanent worker.

- Create a new employee record for them.

- From the Employees tab, select Create Employee.

- Enter their personal details as normal.

- In the Employment Details section, enter the details as normal.

- In the Previous Tax Details section, select the Starting Basis drop-down.

- Select Employee Declaration: P46 - Select category

- Enter the P45 details as required.

- Save your changes.

▼Correcting an incorrectly marked worker Have you marked an employee as deemed who isn't? You need to correct any affected pay runs. Correct the pay runs in date order, the oldest first. - From the Employees tab, select the required employee.

- Clear the Deemed Employee checkbox and Save your changes.

- From the Pay Runs tab, select the first pay run you need to correct.

- Select Edit Pay Run, and tick the box.

- Select confirm.

- Select the required employee, then select their employee name.

- Clear the Deemed Employee check box and select Save.

- If required, add their Student Loan deduction and any absences. Complete the pay run as normal.

- This can change the amount paid to the employee. Select show the difference in the next pay run. This will add or deduct any under or overpayment in the next pay run. For an explanation of this, read the article Correct a completed pay run.

- IMPORTANT - Repeat the process for each affected pay run in date order (oldest first).

Disclaimer This is general rather than specific guidance to assist all of our customers. We always do our best to make sure that the information is correct but as it's general guidance, we make no guarantees concerning its suitability for your particular need. The information is valid at the time of publishing and is provided without any warranty of any kind, express or implied. Take professional advice if you require specific guidance on your individual circumstances, for example to ensure that the results obtained from using our software comply with statutory or regulatory requirements. For Employers, PAYE, NIC, and general tax enquiries, call the HMRC helpline on 0300 200 3200. Visit their website at www.gov.uk. In no event, will we be liable to you for any direct, indirect, consequential or incidental loss or damage arising out of or in connection with your use of the information provided. |