Domestic reverse charge applies when you buy and sell certain goods and services, mainly mobile phones, and computer chips. This article explains how to record the VAT on sales and purchases for goods and services, under the domestic reverse charge rules. What is VAT domestic reverse charge? A domestic reverse charge means the UK customer who receives supplies of mobile phones or computer chips must account for the VAT due on their VAT return, rather than the UK supplier. Usually, when you sell goods or services to another VAT registered business, you include the VAT on your invoice and account for it on your VAT Return. With reverse charge, you do not charge VAT on the sales invoice, although you do have to specify the VAT value and that the reverse charge rules apply. The business that buys the goods or services declares both the purchase and sales VAT. For example, you sell £1,000 worth of mobile phones to your customer, Baker and Company. You do not charge VAT on the invoice. Baker and Company enter the purchase of the mobile phones and adds the £200 VAT to both Box 1 (sales) and Box 4 (purchases) on their VAT return. Reverse charge sales list From 1 July 2022, if you sell mobile phones or computer chips in the UK, you no longer need to compile and submit a Reverse Charge Sales List to HMRC. VAT domestic reverse charge sales Set up customers You must specify that VAT Reverse Charge applies on the sales invoice for those customers who buy mobile phones and computer chips from you. To do this -

Select Contacts, then Customers and open the relevant customer record. -

Select the Options tab, then select the VAT Reverse Charge checkbox. For a new customer, select the checkbox from the Customer Details section. Enter sales invoices If you've set the customer up to use domestic reverse charge, a checkbox shows on the invoice. - Select Sales, then Sales invoices and New Invoice.

- Choose your customer, then select the Use VAT reverse charge checkbox when the reverse charge rules apply.

- Enter the details of the invoice as normal and select the usual VAT rate for these goods. In most cases this will be the standard VAT rate.

-

The VAT analysis section shows that the reverse charge rules apply and reverses the VAT value. - Select Save.

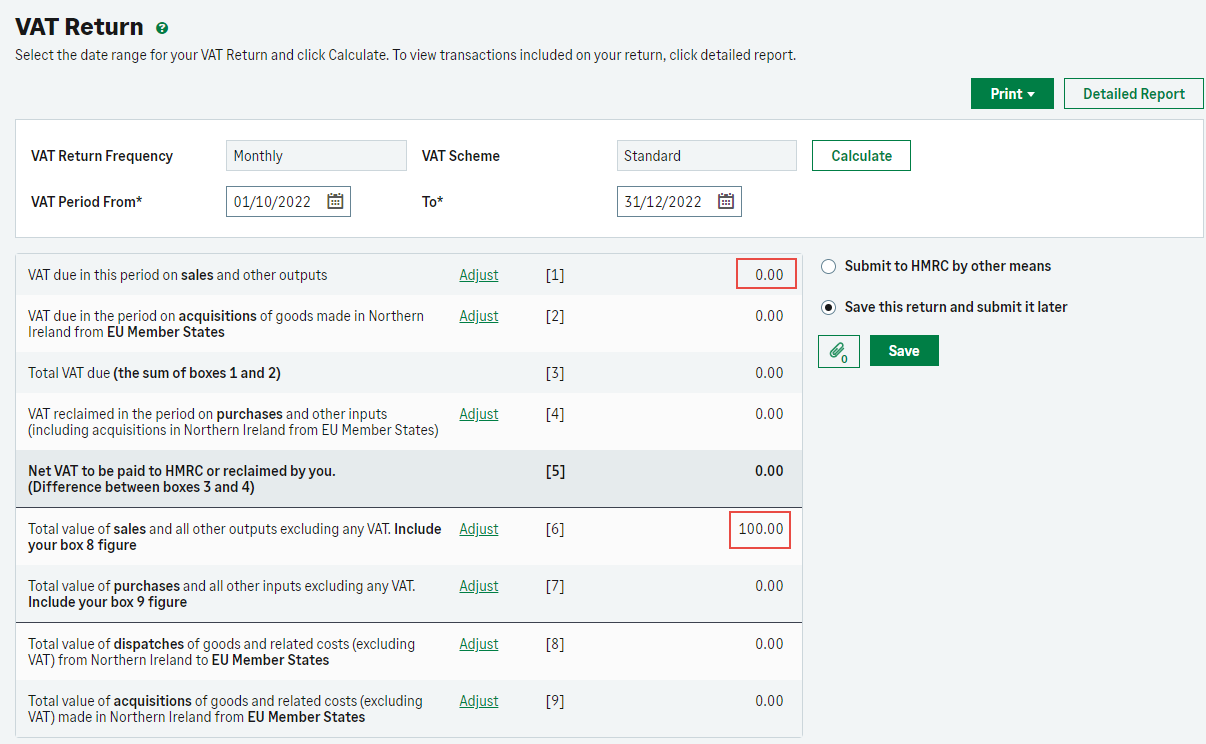

The VAT Return The effect on the VAT return is: - The net value of the sale shows in box 6 as normal.

- The VAT does not show in box 1.

VAT Cash Accounting If you use the VAT Cash Accounting scheme, any invoice where reverse charge applies shows on your VAT Return when you raise it, rather than when your customer pays it. Flat Rate VAT If you use the Flat Rate VAT scheme, any invoice where reverse charge applies shows in the box 6 figure, but not in the flat rate calculation. VAT domestic reverse charge purchases Set up suppliers You need to specify that VAT Reverse Charge applies, for those suppliers who you buy mobile phones and computer chips from. -

Select Contacts, then Suppliers and open the relevant supplier record. -

Select the Options tab, then select the VAT reverse charge checkbox. For a new supplier, select the checkbox from the Supplier Details section. Enter purchase invoices If you've set the supplier up to use domestic reverse charge, a checkbox shows on the invoice. - Select Purchases, then Purchase invoices and New Invoice.

- Choose your supplier, then select the Use VAT Reverse Charge checkbox when the reverse charge rules apply.

- Enter the details of the invoice as normal and select the usual VAT rate for these goods. In most cases this will be the standard VAT rate.

- The VAT analysis section shows that the reverse charge rules apply and reverses the VAT value.

- Select Save.

The VAT Return The effect on the VAT return is: - The VAT shows as a sale in box 1 and a purchase in box 4, which makes the total amount payable 0.00.

- The net value shows in box 7 as normal.

VAT Cash Accounting If you use the VAT Cash Accounting scheme, any invoice where reverse charge applies shows on your VAT Return when you raise it, rather than when you pay it. Flat Rate VAT If you use the Flat Rate VAT scheme, any invoice where reverse charge applies shows in your flat rate, regardless of the value. [BCB:299:UKI - Personal content block - Dane:ECB]

[BCB:302:UKI - Search override - Accounting UK:ECB]

[BCB:276:UKI - hide back button:ECB]

|